Generative-AI apps didn’t just trend in H1’25: they redefined mobile economics. Downloads of AI assistants and AI content tools reached roughly 1.7B while in-app purchase (IAP) revenue hit ~$1.9B, doubling vs. H2’24. That growth was powered by heavyweight launches (ChatGPT, Gemini, Grok, Meta AI) and aggressive paid acquisition.

Here’s the twist for UA managers and publishers: most AI apps monetize through subscriptions/IAP, not ads. So they soak up demand (more advertisers bidding), but add little supply (few ad-supported impressions). The result is tightening auctions across in-app inventory and a playbook shift for anyone buying or selling mobile media.

What Changed in H1’25

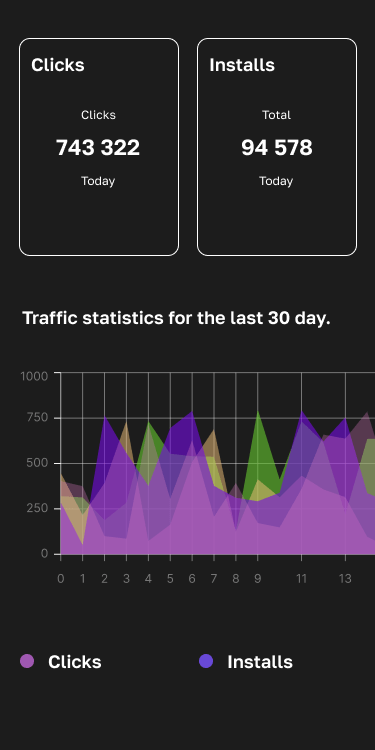

- The category went mainstream. AI app downloads and IAP accelerated to new highs; North America led IAP ($762M), while Asia drove the fastest install growth (+80% vs. H2’24) as AI assistants spread beyond early adopters.

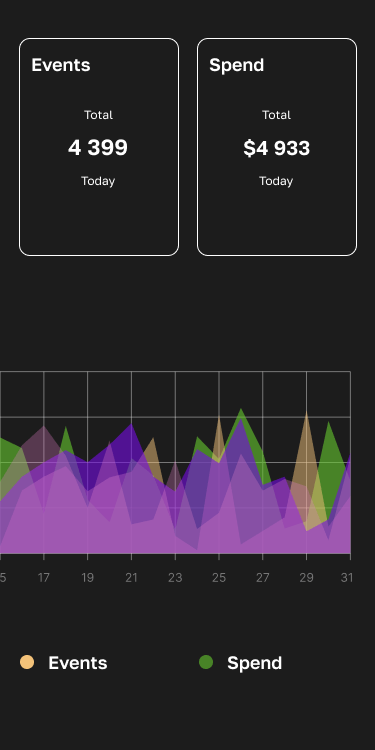

- Budgets followed attention. US digital ad spend by AI brands topped $200M in Q2’25, more than double YoY, as assistants moved from organic buzz to scaled UA.

- Macro tailwinds for IAP. Mobile IAP across stores hit a quarterly record in Q1’25, confirming consumers are comfortable paying in apps, fuel for subscription-heavy AI players.

- 2025 outlook stays bullish. Independent trackers expect >$2B consumer spend on AI apps in 2025, suggesting the competitive pressure won’t fade.

Inventory economics: Why your eCPMs feel different

- Demand up, supply flat. Subscription-first AI apps pour money into UA but rarely run ads themselves. That raises bid density (more buyers per impression) in other categories’ inventory—especially productivity, utilities, education, art/photo, and casual gaming placements where AI advertisers prospect. Expect stronger clearing prices during US/IN/BR dayparts as AI campaigns scale. Evidence: AI brand spend surged while the category’s IAP doubled, signaling high LTVs that justify aggressive bids.

- Geo mix is shifting. Asia’s install outperformance pulls budgets toward India/SEA, while North America remains the IAP profit center (and thus the highest bids). Plan for regional eCPM bifurcation: more pressure in NA premium supply, rising competition in Tier-2 APAC where AI apps chase cheap reach.

- Creative pressure is real. AI brands iterate fast and lean into visual “wow” (image generation, playful animals, everyday utility). Your ads now compete against high-velocity, novelty-rich creatives—click-through lifts translate into higher effective bids.

UA strategy: How to win when AI advertisers crowd the auction

Calibrate bids to lifetime value, not CPI. If your LTV curve can’t stretch to match AI’s subscription economics, shift from broad prospecting to high-intent supply (contextual placements, search/social intent, OEM/on-device) to protect ROAS while AI brands flood open inventory. Use value-based bidding where available, and cap by geo/daypart where AI pressure is highest.

Exploit creative angles AI can’t own. AI assistants sell capability; you can sell outcomes. Anchor concepts in social proof, guarantees, and post-purchase moments (what life looks like after using your app). Maintain a weekly creative ops cadence; AI brands refresh constantly. (Benchmarks show creative velocity is now a performance lever, not a vanity metric).

Sequence owned + paid. When auctions heat up, move first with owned media (push/email/in-app) to capture near-term intent, then use paid for holdouts/longer windows. This reduces exposure to peak eCPMs while preserving volume.

Diversify channels. AI spend spikes aren’t uniform; Sensor Tower flags market-by-market variance. Probe LinkedIn for pro use cases, YouTube/short video for demos, and retail media for commerce-adjacent use. Keep a test-and-learn lane for rising geos where AI apps are scaling installs but pricing hasn’t caught up.

Publisher/mediation Playbook: Monetize the surge

- Tighten floors with data. If you see fill intact but eCPM volatility, raise floors in NA/UK/DE/JP primetime and on high-viewability placements (rewarded/interstitial), then roll back where latency or ARPDAU slips.

- Prefer bidders with AI demand. Ensure your mediation connects to exchanges/networks capturing AI-brand campaigns (check your demand-source mix and line-item win rates). Use A/B waterfalls to validate lift before global rollout.

- Protect UX. AI budgets lift revenue, but novelty creatives can spike frequency. Enforce sensible caps and apply brand-safety filters on UGC-heavy channels.

- Package inventory contextually. Create PMP deals around utility/productivity audiences and high-attention surfaces; AI advertisers pay for context and quality when they scale beyond open auctions.

Creative & measurement tactics that travel well

- “Resume task” deep links. If your ad promises an outcome, land users on a prefilled state or saved progress to offset higher click costs.

- Micro-proof in first 5 seconds. Borrow from AI brands’ show-don’t-tell style: rapid demos, animated before/after, or one-tap “try it.” (Yes, the animal/visual-play trend is real).

- Holdouts > heuristics. When external pricing rises, only incrementality testing (geo/PSA) reveals if your extra spend moved the needle.

- Budget guardrails. Use CPE/CPO and D7/D30 ROAS as gates; pause lines that don’t clear thresholds during AI spend spikes, re-enter in softer dayparts/regions.

H1’25 proved AI apps can buy at scale and monetize at scale – 1.7B installs and ~$1.9B IAP, and their paid budgets are now reshaping auctions. For UA managers, the antidote is value-based bidding, owned-then-paid sequencing, and relentless creative iteration. For publishers, it’s smarter floors, the right demand sources, and contextual packaging. Either way, assume AI pressure persists through 2025 as consumer spend on AI apps climbs past $2B and advertisers keep outbidding slower movers. Adapt your pricing, mixes, and measurement now or watch your margin get modeled away.