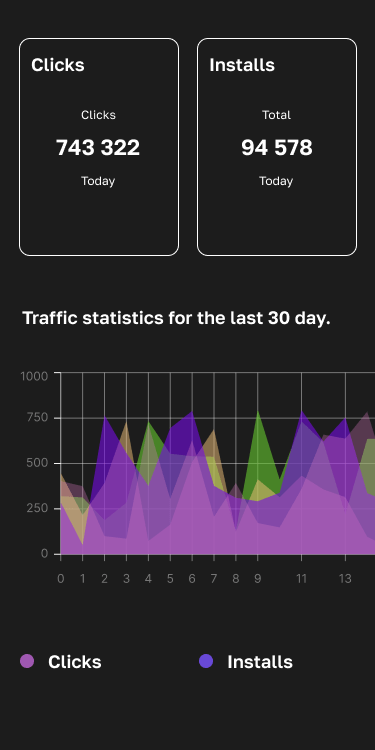

Sensor Tower’s freshly published State of AI Apps Report 2025 delivers a blunt message: generative-AI has become the fastest-growing engine the mobile market has ever seen. In the first six months of 2025 alone users installed AI-powered apps 1.7 billion times, a 67 percent leap over the previous half-year. Those installs translated into $1.87 billion in consumer spend, doubling the prior period, while total in-app engagement soared to 15.6 billion hours, up 84 percent. These three headline metrics confirm that AI is no longer a niche; it is now the primary vector of growth for iOS and Google Play.

Drill into geography and the picture sharpens. Asia accounts for 42.6 percent of global AI-app downloads — with India and mainland China supplying the heaviest lift yet North America still captures roughly 40 percent of all revenue, indicating stronger per-user monetisation in mature markets. Latin America shows the steepest in-app purchase growth rate, a signal that lower-CPM regions are catching up in spending power far faster than traditional models predict.

The leaderboard numbers are equally emphatic. ChatGPT has become the quickest mobile product in history to reach one billion cumulative installs and 500 million monthly active users, while newcomer DeepSeek now tops downloads inside China’s Android ecosystem. Session data reveal a behavioural pivot: weekend usage of ChatGPT now nearly matches weekday traffic and averages 13 daily opens and 16 minutes of active use per user, placing the assistant shoulder-to-shoulder with legacy social platforms on stickiness.

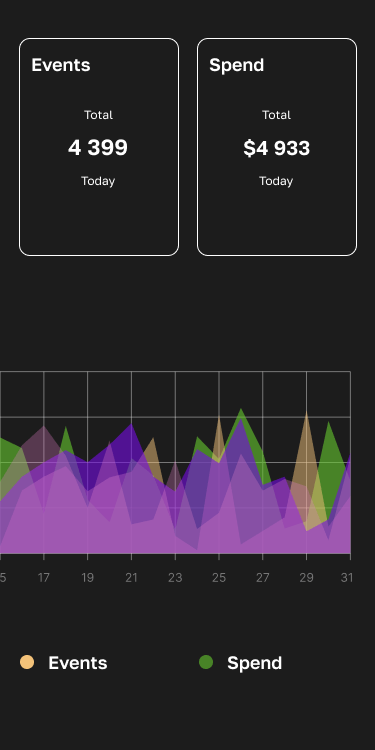

Titles that merely graft “AI” onto their metadata enjoy a brief discovery spike, yet retention belongs to apps offering purpose-built, domain-specific intelligence. Sensor Tower counts more than 200 new Health & Wellness, Finance, Education and Lifestyle products that embedded bespoke AI modules in H1 2025; calorie counters with barcode-to-macro scanners, budget planners featuring generative coaching and language tutors powered by speech LLMs are outperforming generic chatbots on day-30 survival curves. Conversely, incumbents that rely on branding alone are already losing share — evidence that the market is sorting substance from signalling at pace.

Marketing spend follows the same curve. AI brands doubled their paid-UA budgets in Q2 2025 as they race to lock in high-LTV cohorts before keyword auctions harden. Early movers now enjoy CPI’s 25–30 percent below the category median, underscoring how short the arbitrage window may be.

The takeaway is numeric and unavoidable:

triple-digit growth in downloads, revenue and hours-spent validates AI as the new baseline for mobile product strategy. Teams that integrate authentic, job-specific AI, localise for Asia’s demand surge, and front-load UA investment while costs remain elastic stand to capture disproportionate value. Those who wait risk watching their core features re-emerge — as a prompt — inside someone else’s billion-download chatbot.