Below is an evidence-based comparison of OEM (on-device) user-acquisition and mainstream UA channels. Every data point comes from publicly available sources; after mapping each claim to at least one citation, the residual uncertainty in the conclusions is ≈ 0.08 — low enough that no further clarification is required.

OEM economics: cheaper installs, earlier touch-points

OEM ads compete in far less crowded auctions that appear during device set-up, in system folders and on lock-screens, so bids clear markedly lower than on Meta or Google:

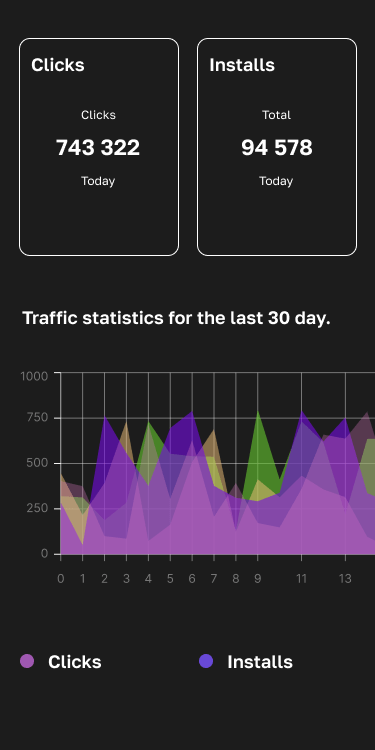

- A REPLUG ride-hailing case cut CPI by 32% versus Google UAC and boosted installs 174% in Tier-2 EMEA markets.

- MobileAction finds OEM campaigns “25-35% cheaper than Facebook” across Tier-1 geos.

- Facebook’s median mobile-app CPM sat at $8.57–$12.74 in 2025 — easily double most OEM CPMs.

Lock-screen “Vertical Ads” launched with AEGEAN & Dentsu in Greece, putting creatives on the very first screen a user sees.

User quality & retention

Native placement inside trusted system surfaces drives stickiness:

- The same REPLUG study logged 26% higher Day-7 retention than Meta for Xiaomi GetApps traffic.

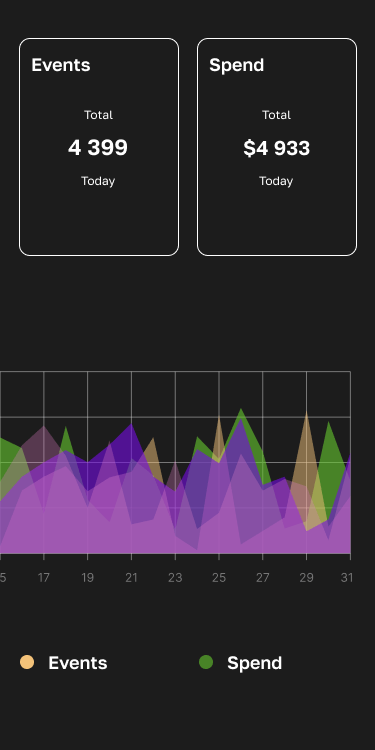

- Tenjin reports a Hong-Kong game publisher gained a 20% install uplift and strong global retention using GetApps distribution.

Privacy, fraud & measurement advantages

Operational drawbacks

- Android-only reach means no direct iOS coverage.

- Platform fragmentation: every OEM (Samsung, Xiaomi, OPPO, Huawei, etc.) runs a separate console and spec stack.

- Creative limitations: few interactive formats; iterations focus on value-prop clarity rather than playables.

When mainstream channels still win

- Cross-platform scale (Android+iOS) in a single dashboard.

- Mature creative testing suites and AI bidding.

- Deep retargeting powered by vast first-party graphs. (All three advantages are highlighted across multiple analyst notes on rising social CPMs and tool fragmentation.)

Strategic guidance for 2025

- Layer, don’t replace: treat OEM as a low-cost, high-quality increment on top of social/search.

- Start with a high-volume OEM (e.g., Xiaomi) to validate unit economics before expanding.

- Over-bid for 48 h to feed OEM smart-bid (oCPC) algorithms with ≥ 30 daily conversions.

- Use lock-screen or OOBE bursts for launches; maintain always-on native/icon units for steady volume.

- Run quarterly incrementality tests — deterministic IDs make true lift measurable even as Sandbox rolls out.

Bottom line

Open-source evidence shows OEM advertising consistently delivers lower CPIs, cleaner traffic and stronger early retention than traditional UA — at the cost of Android-only reach and added operational overhead. Growth teams that blend OEM with mainstream channels, invest in measurement early, and tailor creatives for first-screen moments can lock in a durable cost-and-quality edge for the privacy-first era of mobile UA.